The Promising Growth of the Live Cell Imaging Market in 2019

Live cell imaging technologies have become an essential component of life science research on a global scale. Over the years, live cell imaging technologies have become easier to use for customers to conduct their research, such as drug discovery. Also, the market’s consumables and aftermarket products have experienced an increase in demand due to their multiple uses in various research environments, such as for the creation of 3D cell modeling and measurement of a cell’s health over time.

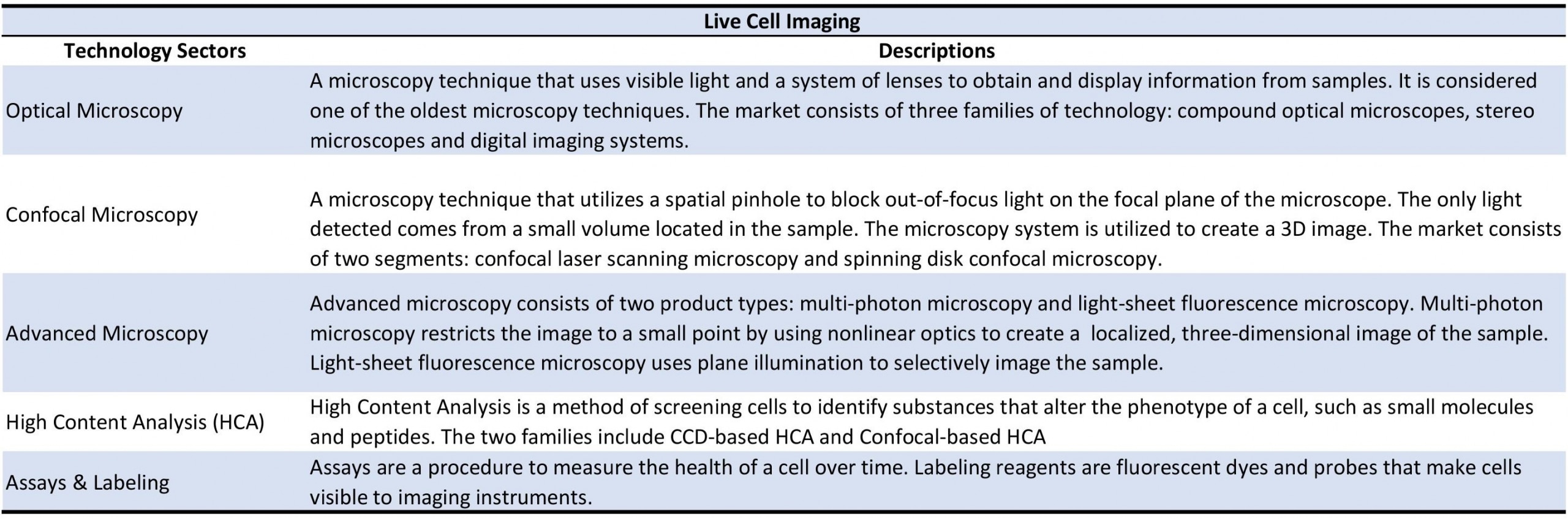

In November 2019, IBO’s publisher, Strategic Directions International, released the “2019 Market for Live Cell Imaging” report, which examines trends, and regional and industrial demands of the live cell imaging market. The report categorizes live cell imaging instruments into five technology sectors: optical microscopy, confocal microscopy, advanced microscopy, high-content analysis, and assays & labeling. Also, the report outlines the leading companies offering these technologies, which include Leica Microsystems (Danaher), ZEISS, Nikon, Thermo Fisher Scientific, Olympus and others.

According to the report, in 2018, the live cell imaging market was estimated at over $1.3 billion and is projected to achieve high single-digit sales growth reaching $1.9 billion by 2023. Advanced microscopes, high-content analysis systems and optical microscopes will account for most of the systems shipped.

The advanced microscopy, and assays & labeling technologies are forecast to be the two fastest growing sectors, with sales for both rising in the high single digits by 2023. Leica Microsystems, ZEISS and LaVision BioTec are the leading companies that provided advanced microscopy products, while Bachem, Essen and Thermo Fisher are the leaders in the assays & labeling business.

Within the advanced microscopy technology sector, multi-photon and light-sheet microscopy technologies are the primary revenue drivers due to vendors introducing improved commercial systems. Also, service and aftermarket products contribute to this technology sector’s market revenues. The imaging assays & labeling reagents technology sector encompass the highest percentage of live cell imaging consumables, with imaging assays representing a fifth of the consumables sub-market. The demand for labeling reagents stems from ongoing innovation.

Geographically, in 2018, the US and Canada, and Europe were the two largest regional markets for live cell imaging technologies, with China being the fastest growing region. All of these regions experienced high demand from the academic, pharmaceutical and life science end-markets. The report forecasts that all three regions’ sales growth will rise in the high single digits by 2023.

End-market wise, the pharmaceutical/biotech, academia and government end-markets accounted for the most live cell imaging sales in 2018. Both the academic and government end-markets utilize live cell imaging tools to study cellular processes and record qualitative data. While the pharmaceutical/biotech sector uses the technology to conduct biopharmaceutical therapeutic drug development, the report also states that the demand for live cell imaging tools will increase in hospitals and clinics due to the application of personalized medicine and cancer treatments.

Between 2017 and 2019, M&A was also a component of sales growth for the live cell imaging market. Bruker acquired the light-sheet microscopy manufacturer LUXENDO for an undisclosed amount in 2017 in order to diversify its advanced microscopy portfolio (see IBO 5/15/17). The next year, Bruker expanded its atomic force microscopy capabilities through the purchase of JPK Instruments, a supplier of biomolecular and cell imaging microscopes (see IBO 7/15/18). This year, BioTek Instruments, a maker of cell imaging plate readers, was acquired by Agilent Technologies for $1.2 billion (see IBO 7/15/19).