Expect More Testing Performed at Physician Office Lab Venues: Report

The IVD market follows patients where technologies allow. There’s no greater evidence for need for IVD product makers to find a market in physician office labs than the declining hospital bed count. With declining hospital bed in developed countries and slow growth in hospital bed volume even in developing nations, it makes sense that more of testing will be shifted in venue to the point of care. Physicians’ offices have evolved into a sizable specialty market served by in vitro diagnostic (IVD) companies. [ https://kaloramainformation.com/product/physician-office-in-vitro-diagnostic-ivd-test-markets/] Our latest report projects IVD product sales of over $8.3 billion in 2022. Over the next several years, the following trends and factors will impact the value and volume of physicians’ office testing activities implemented worldwide.

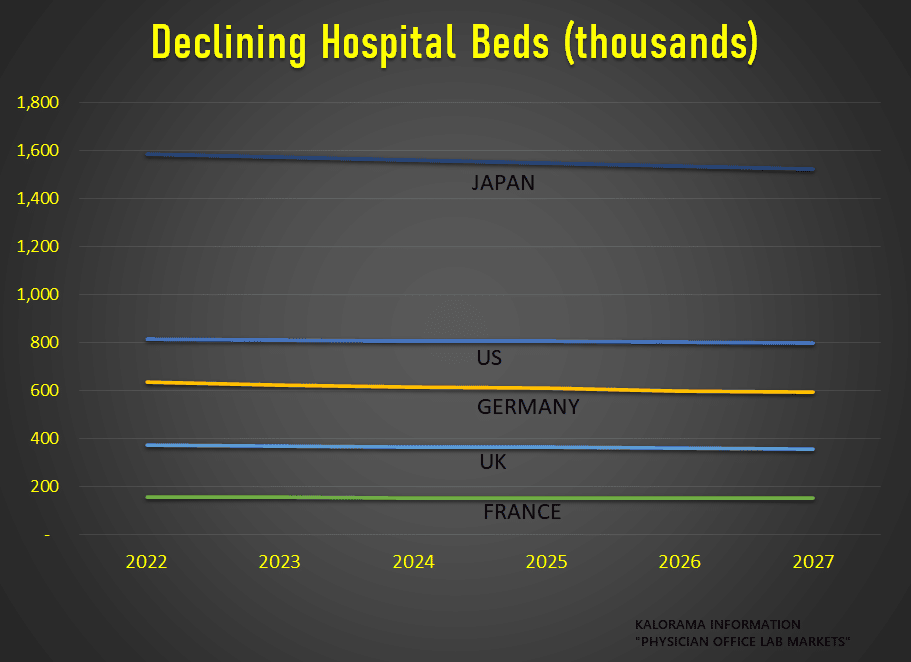

The availability and accessibility of hospitals within a country are best measured by the number of inpatient beds in operation. Most developed countries incorporate an adequate supply and distribution of hospital beds, with some, such as France, Germany, Japan, and South Korea maintaining a surplus capacity. By contrast, the majority of developing countries experience shortages and imbalances in hospital beds. Exceptions include Russia and a number of other East European countries, Brazil, China, and Turkey. These countries have a comparatively high number of hospital beds measured against population. However, a large percentage of these beds are located in old, technologically deficient facilities with limited treatment capabilities. The number of acute care hospital beds in operation worldwide is projected to total slightly more than 19.9 million in 2027, up just under 1.0% annually from 2022. This is anemic growth, if it were not for the availability of other venues such as the physician office, the outpatient center and the home.

The report says 770 million world physician office visits will occur in 2023, providing ample opportunity for testing. This figure does not include urgent care centers, though Kalorama’s report computes a separate market size and forecast for that figure.

Driving physician office lab IVD revenue growth is:

• The increase in numbers of diseases for which the physician office is often first to test – COVID-19, cancer, hepatitis, influenza, malaria clamydia, HIV, tuberculosis and pneumonia.

• advancing IVD technologies will increase the range of diseases and disorders adaptable to physicians’ office testing.

• a gradual easing of pandemic pressures declining, along with increasing competition from self-testing products, will lead to a steady reduction in the number of COVID-19 tests implemented by physicians’ offices.

• the increasing availability of point-of-care (POC) IVD testing in retail establishments and hospital outpatient departments will hold down the overall global volume of traditional physicians’ office testing.

Factors limiting the market include:

• cost pressures from government health programs and health insurance providers will limit coverage and reimbursement rates for physicians’ office tests.

• although growing, the volume of physicians’ office tests implemented in most developing countries will remain comparatively low due to imbalances in the availability and accessibility of healthcare.

• the expanding use of wearable healthcare devices and telehealth services, especially in the developed countries, will hold down the overall volume of physicians’ testing by reducing the number of unnecessary tests.

The report also found that COVID-19 testing products will continue to account for the largest share of global sales, but their overall sales value will decrease steadily as the volume of new cases declines and alternative self-testing products capture away potential applications.

non-COVID Infectious diseases tests, particularly new diseases or diseases for which new tests are introduced will post the second-largest worldwide sales value among IVD products used in physicians’ office laboratories next five years.

The report also found that based on an increasing use in patient physical examinations and wellness checkups, IVD reagents and instruments that measure or detect blood gases, blood-related functions, cancer and cardiac markers, coagulation factors, cholesterol electrolytes, and glucose (including HbA1c) are projected to post steady growth or better in worldwide physicians’ office laboratories.