Point of Care Test Revenue Growth Outpaces Overall IVD Test Market

Introducing accurate test results to the place where patient care is occurring is a compelling concept for improved care. And that is reflected in the growing year-over-year revenues for products that are successful at getting that done. POC has not converted in every category, and it’s not for everything. Indeed, lab-based tests remain stalwart in clinical diagnosis in major market hospitals, where they offer superior sensitivity and specificity and volume advantages.

Yet it the POC market grows larger every year, and 2018 was no exception. This according to Kalorama Information’s latest point of care market study: https://kaloramainformation.com/product/worldwide-market-for-point-of-care-testing/

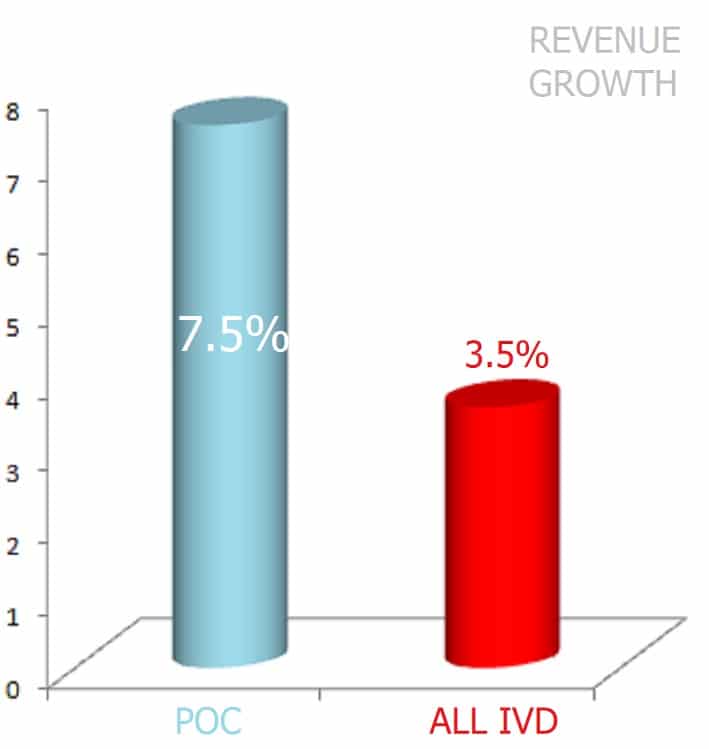

There are cost concerns, there are adoption challenges. And there are technology limitations. But Kalorama finds each year these boundaries are pushed. POC markets grow faster than non-POC markets, and faster than the average of the in vitro diagnostics industry. In 2018, sales of POC testing reached $22.3 billion, increasing 7.5% from $20.7 billion in 2017. That’s fast, more than twice as fast as the whole market grew. New technologies and increased demand contributed to growth in the markets. A contributing factor to slower growth in some segments was pricing strategies that continued to discount the cost of POC diagnostic testing in some segments and higher cost in other segments of testing. In 2023, the total global POC diagnostic testing market is expected to reach $30 billion, displaying growth of 6.1% over the forecast period 2018-2023.

“In 2018, sales of POC testing reached $22.3 billion, increasing 7.5% from $20.7 billion in 2017. That’s fast, more than twice as fast as the whole market grew. “

Diagnostic tests performed outside the central laboratory or decentralized testing is generally known as point-of-care (POC). Over the years, the increasing introduction of transportable, portable, and handheld instruments has resulted in the migration of POC testing from the hospital environment to a range of medical environments including the workplace, home, disaster care and most recently, convenience clinics.

The menu for POC continues to expand. In the past 5-10 years, POC products were developed in the following categories: HbA1c, B-Type Natriuretic Peptide (BNP), whole-blood lactate, D-Dimer, C-Reactive Protein (CRP).

Moreover, POC test devices have contributed significantly to the growth of the overall diagnostics market over the past 10 years. More diagnostic manufacturers have pursued CLIA waiver status for their POC devices and CE Mark for POC or self-use. At the same time more, decentralized test venues invest in non-waived rapid tests and instruments. POC testing appe

ars to be headed for an even bigger role in diagnosis and monitoring patient care. New technologies are allowing POC devices to produce quantitative lab-quality test results that can be transferred automatically to an information system, a remote caregiver service for consultation or an electronic medical record.

Molecular POC tests in physician office are already available for respiratory infections and more. The capacity to provide precise answers for time sensitive tests such as sexually transmissible diseases and other infections will drive the market for POC molecular test devices. Ease of use is a plus for hospital labs. Worldwide, lab budgets are being cut for test send-outs and there are not enough trained technologists to run molecular tests in their present configuration.

Diagnostics are generally a market of focus – the new pharma model tailors therapy to the individual’s particular disease physiology often determined by the results of a diagnostic test. So, more tests – molecular and immunoassays – will come to market, some will have a high price tag and some not. Price will not be the deciding factor. Test adoption in this scenario is based on performance data, contribution to patient outcome and cost/benefit analysis.

A major factor in achieving this goal of more precise and personalized therapeutic options is the use of advanced algorithm driven information technologies that can turn test data into actionable medical decision-making information. This trend is driven by the involvement of major information technology companies and payers that are tired of paying for drugs that often have limited positive patient outcome.

Information about diseases, therapies and tests is readily available via the Internet and a growing number of apps on personal digital assistants (PDAs) including all sorts of smart phones. Wearable devices participate in this area by collecting vital sign data that are then analyzed by IT tools to provide health care improvement instructions.

Kalorama Information’s report can be found at: https://kaloramainformation.com/product/worldwide-market-for-point-of-care-testing/